Wholesale experts TWC Group, in partnership with food-to-go and out-of-home tracking programme MealTrak, has reported the latest food-to-go market performance to 12 w/e 20 February 2023.

Latest results are as follows:

| Latest 52 weeks | 52 weeks (year ago) | 52 w/e YOY change | Latest 12 weeks | 12 weeks (year ago) | 12 w/e YOY change | |

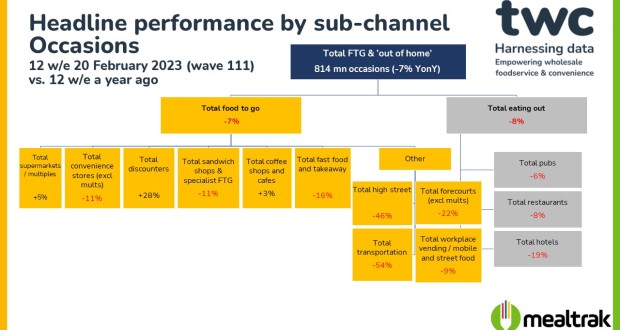

| Total out of home GB occasions | 3.599bn | 3.521bn | +2% | 814mn | 874mn | -7% |

| Total out of home GB Value | £21.631bn | £18.945bn | +14% | £4.991bn | £4.897bn | +2% |

- Latest MealTrak results show the number of out-of-home eating occasions were +2% higher than the comparable period in 2022, on a 52 week/MAT basis.

- However, in the latest 12 weeks, the number of out-of-home eating occasions fell by -7% vs. the equivalent period in 2022.

- In the last 12 weeks, occasions in the ‘eating out’ channel (comprising pubs, restaurants and hotels) declined by -8% vs. the previous year. Pubs continue to outperform the other sub-channels (-6%), ahead of restaurants (-8%) and hotels (-19%).

- Total food to go occasions declined by -7% in the latest 12 weeks. This was driven by transportation sites (-54%), high street (-46%), forecourts (-22%), fast food & takeaway (-16%), sandwich shops and cafes (-11%), independent convenience stores (-11%) and workplace (-9%).

- The multiples (+5%) and the discounters (+28%), with their more affordable food-to-go offer, remain the clear winners. Coffee shops and cafes also recorded modest growth in the latest 12 weeks period, at +3%.

Value sales are up +14% on a 52 week/MAT basis; with a more modest growth rate of +2% on a 12-week ending basis versus 2022.

Commenting on the results, Tom Fender, development director at TWC, said: “Whilst total out of home eating occasions fell by -7% in the latest 12 weeks, this decline is not as deep as the previous period (wave 110), when we reported occasions in decline by -12%. Value sales are in growth (just) on an annual basis, so there is room for cautious optimism.”

“As always, beneath the topline figures, there is a mixed picture. The discounters and multiples continue their long-standing outperformance, whilst coffee shops and cafes have emerged this month with +3% growth vs. the total food-to-go market at -7%, based on occasions in the latest 12 week period.”

“Whilst the out-of-home market continues to face many headwinds, we do see opportunities for those operators that really know their customer and are investing in relevant innovation that meets the needs of the post-pandemic, economically challenged consumer.”

“For instance, we’ve seen a shift in spending into the back end of the week, which represents more leisure-driven occasions, this could well be the driver of the coffee shop occasion, which is an affordable leisure mission.”