Latest results from MealTrak, in partnership with TWC Group, show the number of out-of-home eating occasions were +5% higher than the comparable period in 2021 on a 52 week/MAT basis.

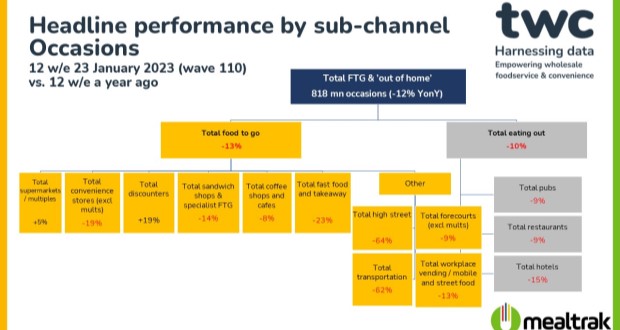

However, in the latest 12 weeks, the number of out-of-home eating occasions fell by -12% vs. the equivalent period in 2021.

In the last 12 weeks, occasions in the ‘eating out’ channel (comprising pubs, restaurants and hotels) declined by -10% vs. the previous year. Pubs have fallen into negative territory this period (-9%), in line with restaurants (-9%) and hotels (-15%).

Total food to go occasions declined by -13% in the latest 12 weeks. This was driven by sandwich shops (-14%), coffee shops & cafes (-8%), fast food & takeaway (-23%), high street (-64%), transportation (-62%), workplace (-13%), forecourts (-9%) and independent convenience stores (-19%).

The multiples (+5%) and the discounters (+19%), with their more affordable food-to-go offer, remain the clear winners, although the growth rate in the mults has slowed this period.

Value sales are up +18% on a 52 week/MAT but have declined by -5% on a 12-week ending basis versus 2021.

Commenting on the results, Tom Fender, development director at TWC, said: “January is typically a tough period for the eating out market, with the cost-of-living crisis adding to the woes of the sector this year.

Occasions fell by -12% vs. January 2021, which is a continuation of the trend of falling occasions that we have been reporting over the last couple of months.”

“Even the multiple grocers with their competitively priced meal deals, have not been immune from the challenges.”

“Whilst still in growth of +5%, this is quite a drop from the double-digit growth we’ve been reporting for some time. The discounters are now the only sub-channel in growth on a 12-week ending basis, and this is from a much lower base, with food-to-go representing a smaller part of the total store offer.”

“January is often a month of good intentions, both from a health and a savings perspective, so the decline in food to go could well be due to increased ‘brown bagging’, with more consumers bringing lunch in from home, or eating at home rather than going out at all.

The biggest mission for food to go – and the fastest growing again this period – remains “something quick & easy to eat”, so this is a key need for operators and suppliers to tap in to.”