Latest MealTrak results show the number of out-of-home eating occasions were -1% lower than the comparable period in 2022, on a 52 week/MAT basis.

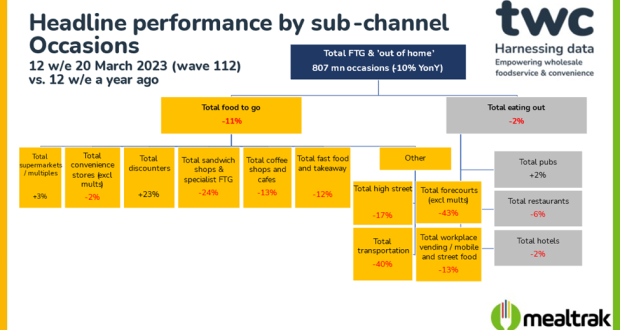

In the latest 12 weeks, the number of out-of-home eating occasions fell by -10% vs. the equivalent period in 2022.

Total food to go occasions declined by -11% in the latest 12 weeks. This was driven by forecourts (-43%), transportation sites (-40%), sandwich shops and specialists (-24%), high street (-17%), coffee shops and cafés (-13%), workplace (-13%), fast food & takeaway (-12%) and independent convenience stores (-2%).

The discounters (+23%) and the multiples (+3%), with their more affordable food-to-go offer, remain the clear winners.

Value sales increased +8% on a 52 week/MAT basis; but were flat (+0%) on a 12-week ending basis versus 2022.

Commenting on the results, Tom Fender, development director at TWC, said: “Out of home eating occasions continued to fall this period, with a decline of -10% in the latest 12 weeks. Interestingly, the ‘eating out’ sector is outperforming food-to-go currently, with a decline of -2% in the latest 12 weeks, vs. -11% for food to go occasions.”

“We continue to see an outperformance amongst those outlets offering more affordable options, namely the discounters – and to a lesser extent the multiple grocers. Discounters saw growth of +23% in the 12 w/e 20 March 2023.”

“Through the cost-of-living crisis, the discounters are performing strongly – with Aldi achieving a record grocery market share of 9.9% in 12 w/e 19 March 2023 and Lidl was the fastest growing supermarket over the same period (Source: Kantar Worldpanel).”

“The impact of the discounters on food-to-go can’t be ignored either. With enhanced ranges and an increase in quality through investment in better ingredients, improved packaging and more sustainable practices, the discounters are offering food to go that is not only affordable, but is also a convenient and credible option.”